When life changes, money changes.

And when money changes, life changes.

Transitions in life aren't just inevitable.

They're constant.

For global clients with increased complexity around their multi-jurisdictional lives...

These crucial moments of transition may shape your entire future.

You've probably been through more than one of 13 these common transitions in the last few years.

They're the common times senior international professionals need our help.

Plus, if you have more than $1.2m to invest, the data tells us a financial planner may just change your life drastically.

1. Retirement

Retirement is one of the biggest life transitions many people will ever make.

Yet most people are not prepared for retirement and need assistance in not only planning for retirement, but also living in retirement.

The vast majority get retirement planning wrong and often only find out far too late.

The key is to identify what you want early on and have a cashflow plan that helps you understand whether or not you're on track.

Retirement planning is a holistic approach that doesn’t just cover you financially, but helps you make better lifestyle choices to achieve your ideal future.

You can start your retirement planning at any point in time; the earlier the better.

2. Divorce

Unfortunately, not all the transitions are necessarily expected, but they happen nevertheless.

There are often legal implications and complexities in an expat divorce and the intersection of emotion and finance during a divorce situation may require outside help.

Even simple things like changing beneficiaries, estate-planning documents, and so on can be difficult to focus on during a stressful divorce.

Couples will likely need to consult with a planner on how to split assets to minimise cross-border tax consequences.

These are just a few of the areas where financial planners can provide value and support.

3. Death of friends or family

The loss of a friend or family member is a difficult time.

In addition to coping with your grief and potentially planning a memorial service or funeral, there are often many financial decisions that follow soon afterward.

This might include dealing with estate plans including trusts and wills, updating financial accounts including beneficiaries on insurance policies and determining how property and assets will be maintained and updated.

4. Changing jobs

Now more than at any time in recent history, massive numbers of workers are considering and seeking a new career path.

Some may adopt a different focus in their current profession, while others may embrace a completely new career.

Every decision you make as part of your career change should be viewed from the lens of your personal financial needs not just for today, but also as part of your longer-term planning needs and goals before. These decisions are acutely important to your long-term financial stability.

A financial planner will help navigate the key financial planning issues that are critical for you to integrate into your career change plans.

5. Losing a job

There will be some obvious turns in your life's journey - job, marriage, children, retirement - that will trigger changes in your financial plans. Then there may be speed bumps such as job loss that will require even more careful handling.

Whether you are asked to leave your job or you quit yourself, the result is the same - a heavy strain on finances.

Even if you haven’t lost your job, now can be a good opportunity to start creating a sound financial plan. This will put your life into numbers and allow you to plan for such events.

6. Moving country

Financial planning for the average investor comes with its fair share of challenges, but tax, retirement, and estate planning become even more complicated when working with senior international professionals whose financial lives cross national borders.

There are also various stages of this transition to consider, such as pre-move, acclimation, global integration and retirement and independence, all of which come with unique financial planning issues.

Whether temporary or permanent, short-term or long-term, expatriate status can present multiple stumbling blocks for financial planning.

7. Buying a house

Even wealthy, well-educated professionals need help during this transition.

Questions arise about the benefits of paying cash instead of securing a mortgage, or what assets to liquidate for a down payment or payment in full.

Then there is the subject of renting versus buying.

These are topics that come up rarely for individuals, but for focused planners they should be easy areas to provide value and expertise.

Take for example an adult child's first home purchase. One key question during this life event centres on whether or not parents should help children with a down payment.

The answer often comes down to the family’s principles, including how parents and children view money or how the parents want the children to view money.

This can be a highly emotional decision.

On the one hand, parents can feel the urge to help, but worry that their kids might develop an unhealthy sense of entitlement. On the other hand, kids can feel like their parents aren’t being helpful enough during a major step in their lives.

A planner can help families sort through this.

8. Receiving an inheritance

A large inheritance can be both a blessing and a burden.

A blessing because the money could be life changing for you and your family and a burden because it imposes a certain responsibility on you to use it wisely and not simply squander it.

A financial planner can help you decide how to handle the money in the short term as well as devise a long-term financial plan that takes all of your assets and obligations into consideration.

9. Selling a business

There are many stages involved in selling a business and some may change/vary depending on the size of your business, where you operate, how you’re regulated and a number of other factors.

These stages involve pre-sale preparation which considers how your business works as a whole, the weak points, the improvements needed and what can be done to make things better. You may need to consider if you need to engage in some form of restructuring to help with the sale.

Another stage will be putting together a summary, teaser or information memorandum, with the assistance of a financial planner. This should be a short document that describes what your business is and the opportunity it represents. It should give enough information to create interest while being anonymous and confidential.

We also work with clients on identifying potential buyers, helping with the bid/auction process and all the necessary due diligence.

10. Ageing parents (and long-term care issues)

This is only going to become a more common transition as the baby boomer generation continues to age.

How should children handle the emotional and financial consequences of taking care of their parents?

Should they keep their parents in their current house or move them to a facility?

What are the financial implications of each situation?

Caring for an ageing parent is one of the hardest transitions that exist and it’s an area where you will need continued financial and emotional advice.

The decisions made during this transition are based on much more than the financial calculations.

Money clouds judgement.

A financial planner steps in during this transition and makes sure everyone is treated with dignity and respect.

11. Illness or death of a spouse

Nobody wants to see a spouse fall gravely ill or pass away.

Both situations are highly emotional, but they also require good financial decision making.

When a severe diagnosis is made, a financial planner will immediately work with the client’s estate-planning lawyer to ensure estate documents and assets are titled in the right way, so the family can be prepared when a tragic event occurs.

Handling sickness and death entails much more than just estate planning; it’s about taking in the entire financial and emotional picture.

These challenges (when an investor’s emotional and financial experiences intersect) require a human element.

In the same way a doctor focuses on limiting anxiety by getting cancer patients to understand the facts about their treatment, a planner can do the same for an investor going through the death of a spouse.

It requires deep subject matter expertise.

12. Legacy issues

Legacy planning isn’t just for the super wealthy.

High-net-worth client need to think about a number of things, like whether the legacy and planning be built around other planning vehicles like charitable lead trusts or charitable remainder trusts.

Other legacy issues are equally as important, regardless of a client’s net worth.

If they have kids, how do they talk to them about money issues?

If charity and giving back to the community is important, how do they continue to use the resources they have to encourage this?

13. Wealth accumulation, deaccumulation and transfer

Accumulation is the period of time when you are accumulating assets. You are working and trying to save and invest for life goals.

Deaccumulation is when the time has come for you to spend the money you have saved and invested. This generally occurs in retirement.

In terms of transfer, this means the time has come for you to transfer money to loved ones and charities, and to pass other legacy items to the next generation.

If you review the other major transitions and other smaller transitions people will go through throughout their lives, they occur in each of these three categories.

One more, compelling reason

So there you have it, 13 reasons you may need a financial planner next year.

As you think of your goals for the coming year, ask yourself why you want to achieve that goal. Now, ask yourself why that is important to you.

You'll find that no matter your goal, eventually these goals are important because you want either yourself or someone you love to be happy.

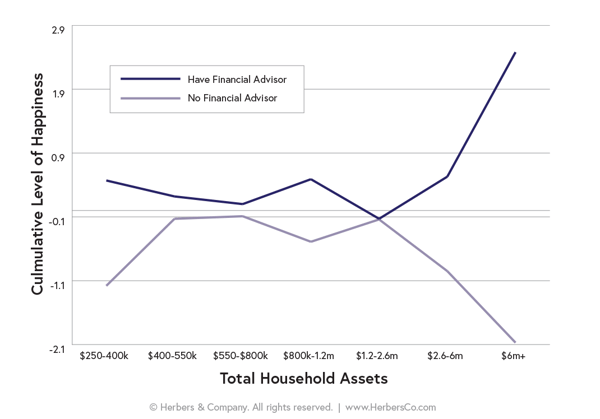

In a recent survey of 1,000 random consumers across the US...

(all of whom had self-reported assets of $250,000 or more),

Researchers found that those with a financial planner were statistically happier than those without one.

This survey identified four core factors that make people happier: fulfillment, intention, impact and gratefulness.

The result?

All four predictors of happiness were heightened among consumers who work with financial planners — by a wide margin.

This held true even when controlling for gender, age, income and asset levels.

But what I found most interesting...

As individuals move past $1.2 million of assets, those who work with financial planners rapidly increase in happiness, while those without planners rapidly become less happy.

So what is the true value of a financial planner?

Yes, they provide investment management advice, financial planning services, and guidance for their clients’ financial futures.

More importantly though, hiring financial planners, sooner rather than later, makes people happier.

In fact, for individuals with more than $1.2 million in assets, a financial planner is critical to happiness.

Every day, families have to deal with crucially important financial decisions and situations that they never dreamed would crop up in their lives.

Their stories are real and often serious.

But for us, successfully guiding clients through the changes and transitions of life requires more than sound technical knowledge and advice.

It's about having a solid relationship and being a financial coach, delivering advice proactively, not reactively.

For every one of us who encounters a divorce, unexpected death or some other triggering point, we should at least be aware of the tools to find the right financial planner who can offer help.

These life events are the financial game-changers.